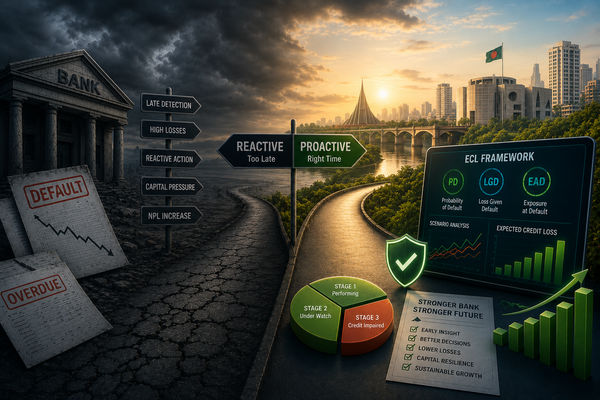

Inside the ECL Engine: How Banks Estimate Future Credit Loss

When people hear “Expected Credit Loss,” they often think of an accounting calculation.

But in practice, ECL is much more than a formula.

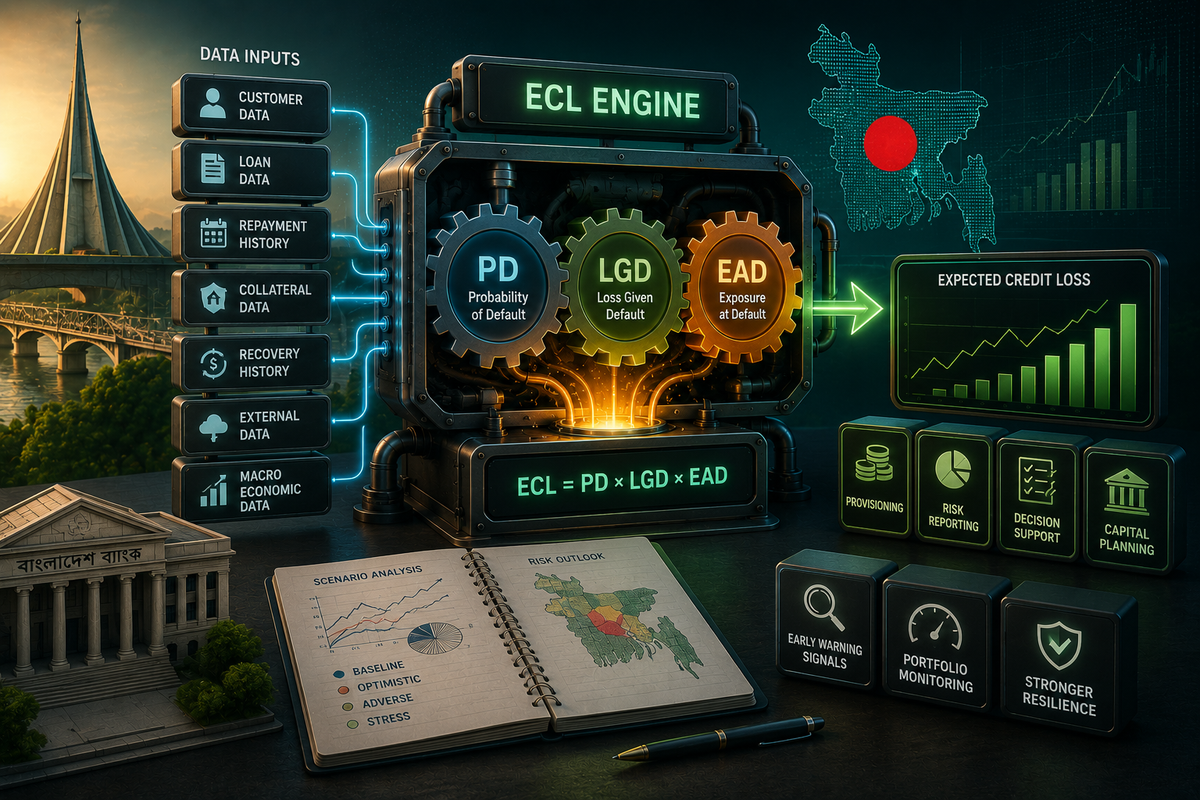

It is a risk prediction framework that brings together data, models, assumptions, economic forecasts, and governance controls to estimate how much loss a bank may face in the future.

At the center of this framework are three important concepts:

PD, LGD, and EAD.

These three components form the foundation of ECL calculation.

The basic idea

At a simple level:

Expected Credit Loss = Probability of Default × Loss Given Default × Exposure at Default

Or:

ECL = PD × LGD × EAD

This formula may look simple, but each component requires strong data and careful judgment.

PD: Probability of Default

PD means the likelihood that a borrower will default within a certain period.

For example, if a borrower has a 3% probability of default, it means the bank estimates that there is a 3% chance the borrower may fail to meet repayment obligations.

PD can be calculated for:

- 12 months

- lifetime of the loan

For a healthy loan, banks usually estimate 12-month expected loss. But if the borrower’s risk increases significantly, the bank must estimate loss over the full remaining life of the loan.

PD depends on factors such as:

- repayment history

- overdue behavior

- borrower financial strength

- industry condition

- credit rating

- macroeconomic outlook

In a modern ECL system, PD should not be static. It should change when the borrower or economy changes.

LGD: Loss Given Default

LGD means how much the bank expects to lose if the borrower defaults.

For example, suppose a bank has given a loan of BDT 10 crore. If the borrower defaults, the bank may recover some amount through collateral, guarantees, or legal recovery.

If the bank expects to recover 60%, then the expected loss is 40%.

That 40% is LGD.

LGD depends on:

- collateral value

- type of collateral

- recovery history

- legal enforcement time

- borrower segment

- loan seniority

- market conditions

A fully secured loan may have lower LGD. An unsecured loan may have higher LGD.

EAD: Exposure at Default

EAD means how much exposure (Exact amount of loss during default) the bank will have at the time of default.

For a term loan, EAD may be close to the outstanding loan balance.

But for products like overdraft, credit card, LC, guarantee, or working capital limit, EAD is more complex because the borrower may use more of the approved limit before default.

EAD considers:

- current outstanding balance

- undrawn limit

- product type

- expected utilization before default

- off-balance sheet exposure

This is why ECL applies not only to funded loans but also to non-funded facilities.

A simple example

Suppose a bank has a corporate loan with:

- EAD: BDT 10 crore

- PD: 5%

- LGD: 40%

Then:

ECL = 10 crore × 5% × 40% ECL = BDT 20 lakh

This means the bank may need to keep BDT 20 lakh as expected credit loss provision for that exposure, depending on the stage and model assumptions.

Why the formula is only the beginning

The formula is simple. The implementation is not.

Banks need reliable data to estimate PD, LGD, and EAD. They need models that can be validated. They need audit trails to explain how the numbers were generated.

They also need scenario analysis.

For example:

- What happens if inflation rises?

- What happens if GDP growth slows?

- What happens if export demand falls?

- What happens if interest rates increase?

These economic assumptions can change PD and LGD.

So ECL is not a one-time calculation. It is a continuous process.

The ECL engine

A practical ECL engine usually includes:

- data collection layer

- data quality validation

- borrower segmentation

- PD model

- LGD model

- EAD model

- macroeconomic scenario engine

- ECL calculation engine

- reporting dashboard

- audit and approval workflow

This creates a complete risk calculation ecosystem.

ECL is not just about calculating a provision.

It is about building a disciplined, data-driven way to understand future credit risk.

For banks, the real value lies not only in compliance, but in the ability to see risk earlier and act faster.