Data Is the Foundation of ECL: Why Banks Must Build a Strong Credit Risk Data Strategy

Most ECL projects do not fail because people misunderstand IFRS 9.

They fail because the required data is missing, scattered, inconsistent, or unreliable.

Expected Credit Loss depends on models. Models depend on data. If the data is weak, the ECL output will also be weak.

That is why data readiness is one of the most critical success factors for ECL implementation.

Why ECL needs more data than traditional provisioning

Traditional provisioning often depends on loan classification, overdue status, and fixed regulatory percentages.

ECL requires much more.

Banks must estimate future losses based on borrower behavior, historical experience, current condition, and future economic expectations.

This requires a broader data ecosystem.

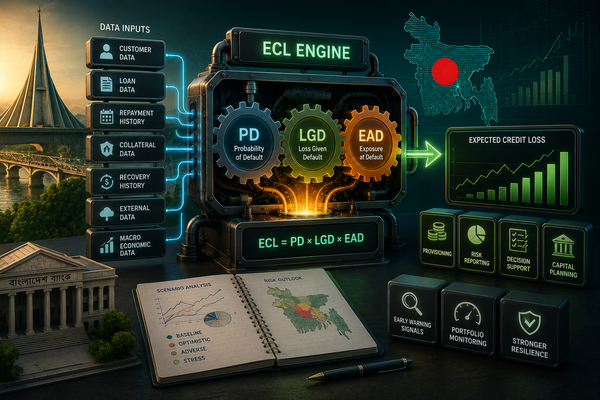

Key data required for ECL

A bank needs data from multiple systems.

Customer data

This includes:

- customer profile

- business type

- industry or sector

- ownership structure

- group exposure

- customer rating

- financial statements

Customer data helps identify who the borrower is and what kind of risk profile they carry.

Loan account data

This includes:

- loan type

- disbursement date

- maturity date

- outstanding balance

- repayment schedule

- installment amount

- overdue history

- restructuring history

This helps determine the current status and behavior of the loan.

Repayment behavior

Repayment history is extremely important.

Banks need to know:

- how often payments were delayed

- how many days past due

- whether the borrower regularized quickly

- whether delays are increasing

- whether repayment behavior differs by segment

This data supports PD modeling.

Collateral data

Collateral affects LGD.

Banks need:

- collateral type

- accepted value

- current market value

- valuation date

- legal enforceability

- recovery history

- collateral coverage ratio

If collateral data is outdated, LGD may be inaccurate.

Recovery data

Banks need historical recovery experience.

For example:

- how much was recovered after default

- how long recovery took

- which collateral types recovered better

- which sectors showed poor recovery

- legal cost and recovery cost

Without recovery data, LGD estimation becomes difficult.

Off-balance sheet exposure

For LC, guarantee, overdraft, and unused limits, EAD calculation requires additional information.

Banks need:

- sanctioned limit

- utilized amount

- undrawn amount

- product behavior

- conversion factor

- customer usage trend

This is important because exposure may increase before default.

Macroeconomic data

ECL is forward-looking. So banks must consider macroeconomic variables such as:

- GDP growth

- inflation

- interest rate

- exchange rate

- unemployment

- sector performance

- commodity price movement

These variables help banks understand how the economy may affect borrower default risk.

Common data problems in banks

Many banks face similar challenges.

Data silos

Credit data may be in one system, collateral data in another, customer data in another, and recovery data in spreadsheets.

This creates reconciliation problems.

Missing data

Important fields may be blank, outdated, or not captured at all.

For example:

- sector code missing

- collateral valuation date missing

- customer rating not updated

- restructuring reason not recorded

Inconsistent definitions

Different departments may define the same thing differently.

For example, “default,” “watchlist,” “restructured,” or “SME segment” may not be consistently used.

Manual reporting

If ECL data is prepared manually, the process becomes slow, risky, and difficult to audit.

Manual Excel-based calculation may work for pilot testing but is not sustainable for full implementation.

What banks should do

Banks should start with a data gap assessment.

They should identify:

- what data is required

- where the data currently exists

- what is missing

- which data is unreliable

- what needs system integration

- what needs governance control

Then they should build a centralized ECL data mart or risk data warehouse.

Data governance

ECL needs strong ownership.

Banks should define:

- data owner

- data source

- validation rule

- correction process

- approval workflow

- audit trail

Without governance, ECL results may be questioned by auditors and regulators.

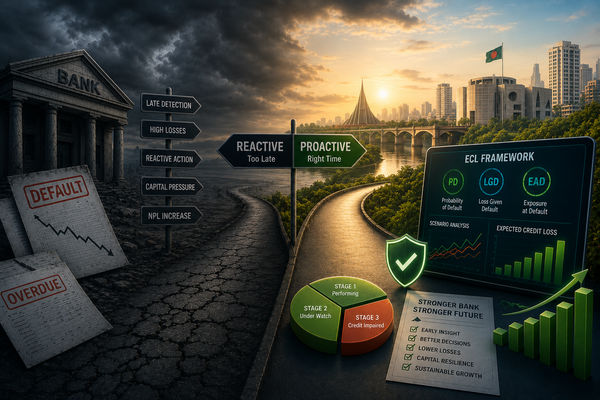

ECL implementation begins long before model development.

It begins with trusted data.

The banks that build strong data foundations today will be better prepared not only for IFRS 9 compliance, but for the future of intelligent risk management.