The Day a Loan Turns Bad Is Already Too Late: Why Bangladesh’s Move to ECL Matters

A borrower rarely becomes risky overnight.

A trading company may continue paying installments on time, while its sales are already declining. A manufacturing client may still look healthy in the core banking system, while raw material prices, exchange rate pressure, or falling export orders are silently weakening its cash flow. By the time the loan becomes overdue, the risk may have been building for months.

This is the problem Bangladesh Bank’s upcoming Expected Credit Loss (ECL) framework is trying to address.

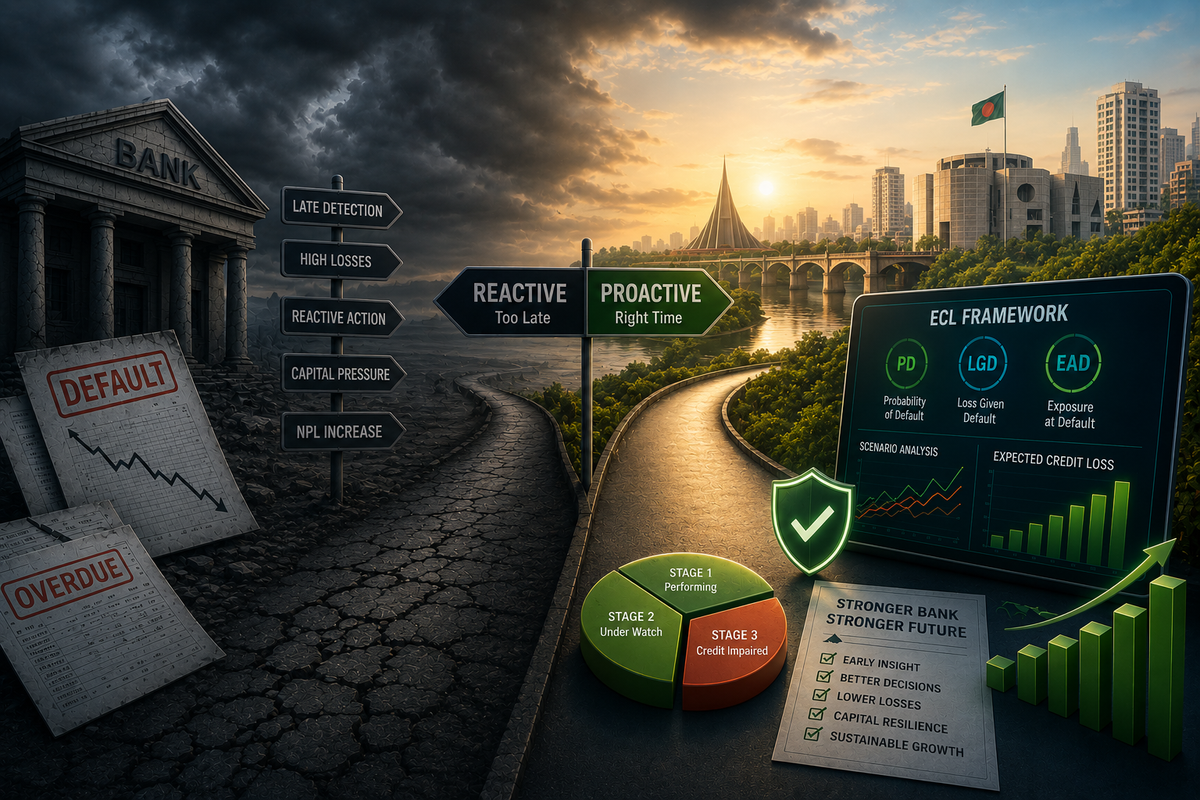

Under the traditional provisioning model, banks usually recognize credit loss after a loan shows visible signs of deterioration. In simple terms, the bank reacts after the damage has already appeared.

ECL changes that mindset.

Instead of asking, “Has this borrower already defaulted?” the new model asks, “What is the probability that this borrower may default in the future?”

That shift may sound technical, but it has major implications for the banking industry.

From reactive banking to predictive banking

The current incurred loss model is backward-looking. It depends heavily on loan classification status and past events. If a loan is performing, the bank may not need to keep significant provision against it. But real credit risk often develops before default.

ECL is forward-looking. It requires banks to estimate possible future losses using:

- borrower repayment behavior

- current financial condition

- historical default patterns

- sector performance

- macroeconomic forecasts

- collateral and recovery assumptions

This means banks will need to monitor risk more continuously, not just during periodic classification exercises.

Why this matters now

Bangladesh’s banking sector is becoming more complex. Loan portfolios are growing, borrowers are exposed to global markets, and economic conditions can change quickly. Inflation, exchange rate volatility, interest rate movement, and sector-specific stress can all affect credit risk.

A traditional provisioning system may not capture these risks early enough.

ECL gives banks a structured way to prepare before the loss becomes visible.

What changes for banks

ECL is not only an accounting change. It affects risk management, technology, data governance, capital planning, and board-level decision-making.

Banks will need to answer questions like:

- Do we have enough historical loan data?

- Can we identify early warning signals?

- Can our systems calculate PD, LGD, and EAD?

- Can we generate scenario-based forecasts?

- Can we explain our models to auditors and regulators?

These questions are not optional. They define whether a bank is ready for IFRS 9-based ECL.

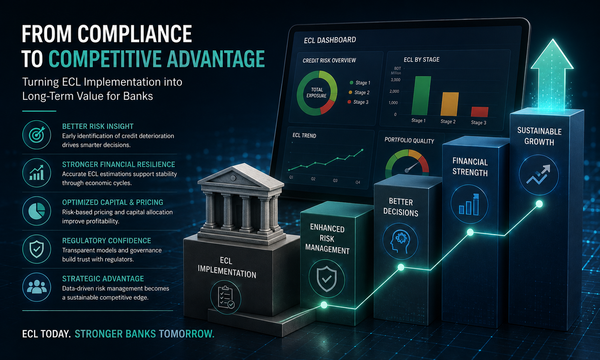

Why early preparation creates advantage

Banks that start early will not only meet regulatory requirements. They will gain better visibility into portfolio quality.

They will be able to identify risky segments earlier, price credit more accurately, and make better capital decisions.

In the long run, ECL can help banks move from compliance-driven reporting to intelligence-driven risk management.

The future of credit risk management is not about discovering bad loans after they become bad.

It is about identifying tomorrow’s risk today.

For Bangladeshi banks, ECL is the beginning of that transformation.