The Three-Stage Journey of a Loan Under IFRS 9

Every loan has a life story.

It starts with approval, disbursement, repayment, monitoring, and eventually closure. But during that journey, the credit quality of the borrower may change.

A borrower may begin as financially strong. Later, cash flow may weaken. Eventually, the borrower may become unable to repay.

IFRS 9 captures this journey through a three-stage credit risk model.

This three-stage structure is one of the most important concepts in Expected Credit Loss.

Why staging matters

Under a traditional system, banks often focus on whether a loan is classified or non-performing.

But risk does not move from good to bad in one jump.

There are warning signs in between.

The three-stage model helps banks identify those warning signs and adjust provisions accordingly.

Stage 1: Performing loans

Stage 1 includes loans where credit risk has not increased significantly since origination.

These are generally healthy loans.

The borrower is paying regularly, and there is no major sign of deterioration.

For Stage 1 loans, banks calculate 12-month ECL.

This does not mean the bank expects the loan to default within 12 months. It means the bank calculates expected loss from default events that may occur within the next 12 months.

Example

A good corporate borrower takes a term loan.

The borrower has a strong repayment history, stable cash flow, and no overdue record.

This loan remains in Stage 1.

The provision requirement is comparatively lower.

Stage 2: Significant increase in credit risk

Stage 2 is where things become more important.

The loan is not yet defaulted. The borrower may still be paying. But risk has increased significantly compared to the time of loan approval.

This is the early warning zone.

Possible indicators include:

- frequent payment delays

- declining sales

- weak cash flow

- downgrade in internal credit rating

- sector-level stress

- high leverage

- restructuring request

- adverse market conditions

For Stage 2 loans, banks calculate lifetime ECL.

This means the bank estimates expected loss over the remaining life of the loan, not just the next 12 months.

Why this is important

Stage 2 is where ECL becomes powerful.

It allows the bank to recognize risk before default happens.

This gives management time to act.

The bank may increase monitoring, reduce exposure, request additional collateral, revise limits, or restructure under proper policy.

Stage 3: Credit-impaired loans

Stage 3 includes loans that are already impaired or defaulted.

These are problem loans.

The borrower may have missed payments, become non-performing, or shown clear evidence of financial distress.

For Stage 3, banks also calculate lifetime ECL. However, interest income treatment changes.

Instead of recognizing interest on the gross loan amount, interest is calculated on the net carrying amount after deducting loss allowance.

This gives a more realistic picture of income.

A simple borrower journey

Imagine a textile exporter.

At loan approval, the company has strong export orders and a good repayment history.

Stage 1

The borrower is performing normally.

Stage 2

Global demand slows down. Export orders fall. Cash flow becomes tight. Installments are still paid, but sometimes delayed.

The loan may move to Stage 2.

Stage 3

The borrower misses multiple payments and cannot regularize the account.

The loan moves to Stage 3.

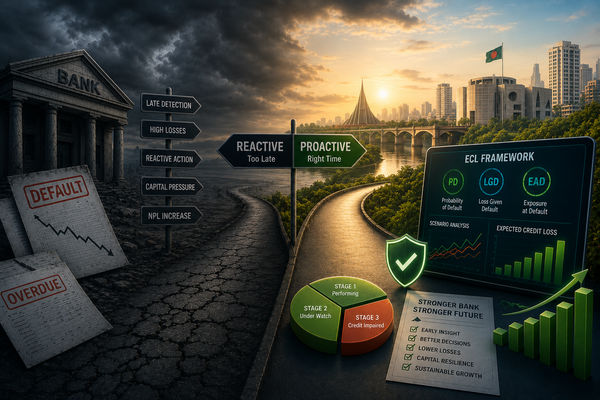

This journey shows why staging is important. It gives the bank a structured way to monitor risk deterioration.

Business impact of staging

The three-stage framework affects:

- provisioning amount

- risk monitoring

- credit review frequency

- portfolio reporting

- capital planning

- management decision-making

It also improves transparency because management can see how much of the portfolio is healthy, deteriorating, or impaired.

Technology requirement

To implement staging properly, banks need systems that can track:

- origination credit quality

- current credit quality

- days past due

- rating changes

- restructuring events

- watchlist status

- sector stress

- collateral changes

Without system support, staging may become manual and inconsistent.

The three-stage model transforms loan monitoring from a static classification exercise into a dynamic risk journey.

A modern bank should not only know which loans are bad.

It should know which good loans are starting to become risky.